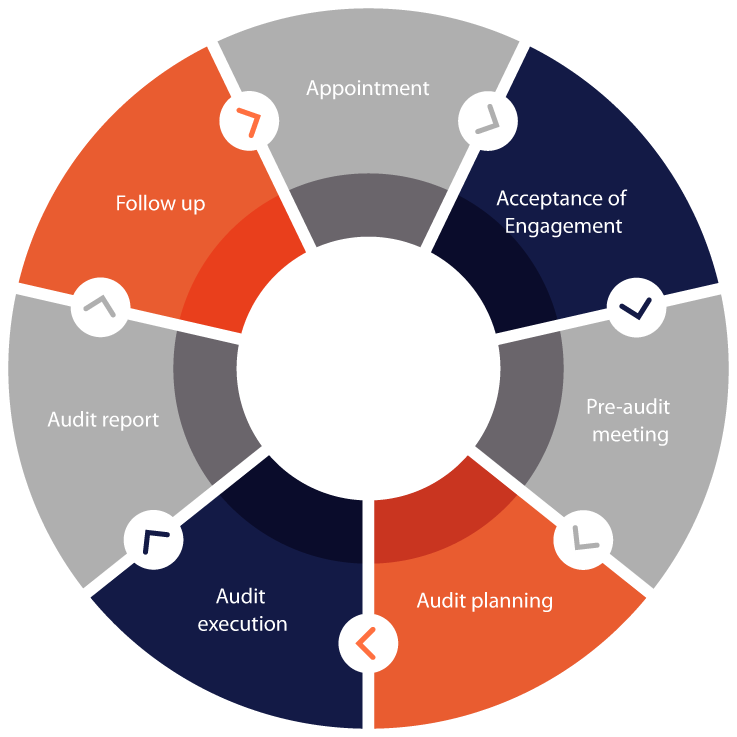

Basic details

Reconciliation of the turnover as per the audited annual financial statement with the one declared in the annual return (GSTR-9)

Tax Payment Reconciliation

Input Tax Credit (ITC) Reconciliation

Auditor's recommendation on additional liability due to non-reconciliation

Study of internal controls

Our auditors study the effectiveness of internal controls and internal checks established by the management to ensure GST compliance. A review of internal controls applicable to transactions like sales returns, sale on approval basis, and job work is also carried out for their completeness and actual implementation. Our GST auditors also study the adequacy of records maintained under GST and provide their recommendations.

records verification

Our GST Auditors verify the GST registration certificate, classification of supplies and services under GST, reverse charge, purchase register, sales register, stock register, expense ledgers, monthly and quarterly returns, and other records maintained by the company as per the requirements of the law.

Our GST Auditors verify the GST registration certificate, classification of supplies and services under GST, reverse charge, purchase register, sales register, stock register, expense ledgers, monthly and quarterly returns, and other records maintained by the company as per the requirements of the law.

cross verification of GSTR-3B to GSTR-1 AND 2A

We cross-check GSTR-3B with GSTR-1 and 2A to ensure that input tax credit has been properly claimed. We also check the arithmetical accuracy of figures and identify mismatch, if any. Based on our findings, we recommend management to make necessary changes.

invoice verification

>We check the outward invoices to ensure that the format of the invoice complies with the law. We then go on to check the arithmetical accuracy of the same and check if the tax rate is correctly charged considering the goods and services supplied.

We also check purchase invoices for their eligibility for input tax credit (ITC) and verify if the total of such ITC matches with the amount of credit claimed in the GST return.

We check the outward invoices to ensure that the format of the invoice complies with the law. We then go on to check the arithmetical accuracy of the same and check if the tax rate is correctly charged considering the goods and services supplied.

We also check purchase invoices for their eligibility for input tax credit (ITC) and verify if the total of such ITC matches with the amount of credit claimed in the GST return.

ICt non-payment reversals

Our GST auditors check if the input tax credit is reversed if the invoice under review has remained unpaid for more than 180 days.

E-way bills compliance check

We check if the e-way bill is generated for each supply having value more than Rs. 50,000 and supplies made via motorised vehicles. They also check if the e-way bill matches the invoice.

We check if the e-way bill is generated for each supply having value more than Rs. 50,000 and supplies made via motorised vehicles. They also check if the e-way bill matches the invoice.

industry-specific check

Some of the GST provisions apply to specific industries. Our GST auditors carry out further examination of the records if specific provisions are prescribed for your industry.